If you have been tracking financial markets, you have likely come across the “sell the fact” adage, suggesting that markets tend to drop after realizing highly anticipated positive developments.

A notable example of the phenomenon would be bitcoin’s 22% slide in two weeks after the much-awaited spot bitcoin exchange-traded funds (ETFs) began trading in the U.S. on Jan. 11.

Now, market watchers may anticipate a similar sell-off in bitcoin as Republican Donald Trump, who, after months of winning over the crypto community by embracing digital assets, is set to return to the White House.

A big sell the fact decline, however, looks unlikely to due following reasons:

Last minute de-risking

The final stretch of the U.S. presidential election campaign was characterized by a sudden spike in Democrat candidate Kamal Harris’ victory odds in crucial swing states like Pennsylvania.

As Harris’ odds picked up in the second half of last week, the so-called Trump trades, involving bullish bets in BTC, the dollar index, and short positions in Mexican peso and government bonds, ran out of steam.

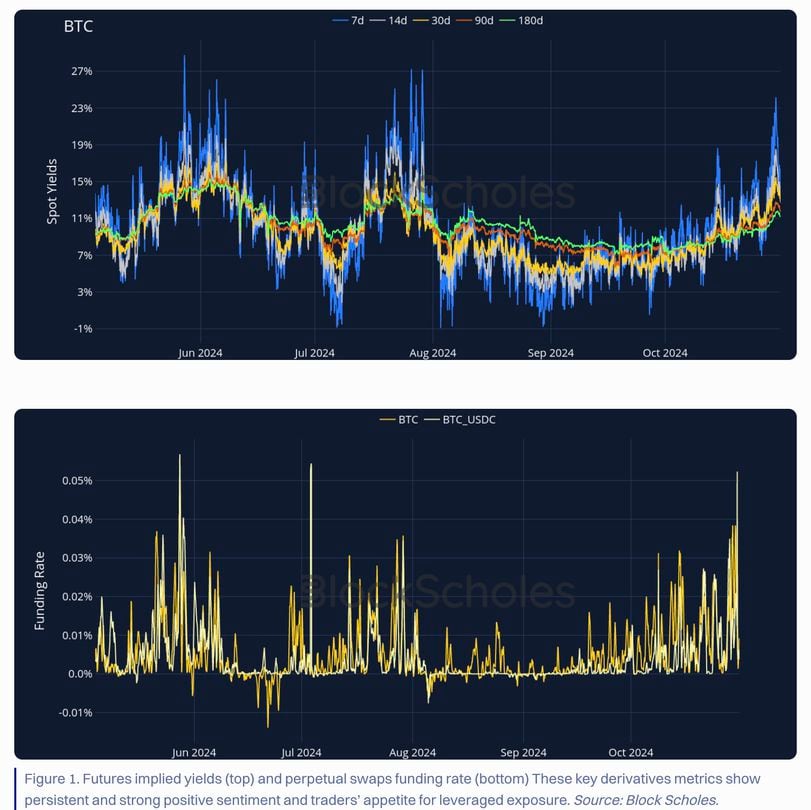

BTC turned lower from the high of $73,400 last Tuesday and probed lows under $66,000 early this week. The price drop flushed out excess leverage that was reminiscent of the January ETF launch, according to data tracked by analytics firm BlockScholes.

The chart shows that the short-duration BTC futures yields or basis surged in October alongside a spike in funding rates, reflecting a bullish leverage buildup as prediction markets pointed to a convincing Trump win.

Both metrics climbed down over the weekend as Trump’s victory became uncertain, signaling a last-minute moderation in the derivatives market activity and setting the stage for a long-lasting bullish action on potential Trump victory.

Additionally, with Harris and Trump running neck and neck over the weekend, traders could not fully commit to pricing in a Trump or Kamala victory. Now that Trump has officially won, traders will likely be more confident in expressing their bullish views.

Absence of “buy the rumor” rally

The key prerequisite for a sell-the-fact price drop is a strong buy-the-rumor rally. Bitcoin never really had it.

Trump began courting the crypto community aggressively in June, taking several steps to win their votes, including promising to launch a strategic bitcoin reserve in a potential second term. Additionally, he launched his cryptocurrency venture, World Liberty Financial and accepted crypto donations. These initiatives heightened hopes that a second Trump administration would bring regulatory relief to the crypto industry, leading to BTC often taking cues from Trump’s election victory odds.

Despite all optimism, bitcoin’s price remained trapped in a broad sideways range, with the upside consistently capped at around $70,000 due to supply overhang fears and macroeconomic factors. And it’s only today that prices have broken out of the prolonged seven-month trading range. In other words, the party looks set to continue without a major hiccup.

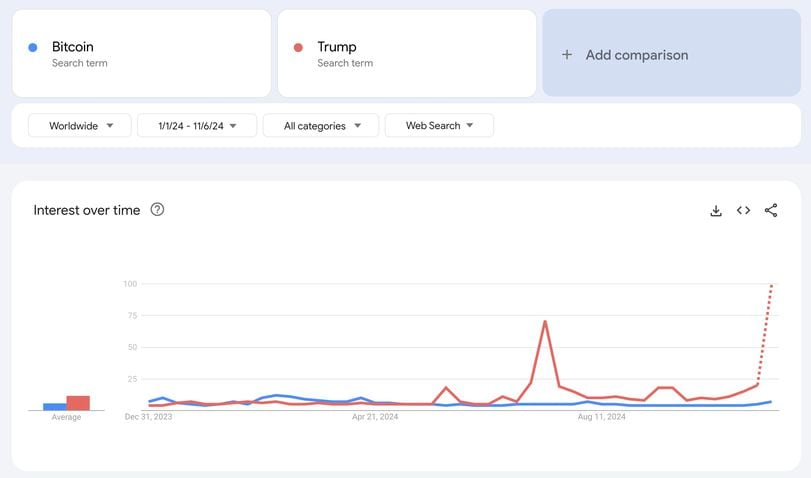

Besides, there is barely any sign of retail investor frenzy, as highlighted by low values in Google search query for the term “Bitcoin” relative to the term “Trump.” A retail frenzy is often observed at notable market tops.

Watch out for the other side of the Trump trade

The other side of the Trump trade involves taking bearish bets on U.S. government bonds (betting on higher bond yields) and betting on gains in the dollar index. This could pose a headwind to risk assets, including cryptocurrencies.

Yields are already rising as Trump has promised to impose sweeping tariffs on China, Mexico and other prominent trading partners in a bid to onshore manufacturing. Tariffs, however, are inflationary in nature and may derail the Fed’s plan to normalize the overly tight monetary policy via rate cuts.

The yield on the 10-year Treasury note has jumped 20 basis points to 4.47%, teasing a move past an 11-month downtrend line. Accelerated gains in the benchmark yield or the so-called risk-free rate could strengthen the dollar and drain capital from riskier assets.