Margin calls are coming for cryptocurrency miners as the bear market continues to claim victims.

The private and publicly listed crypto miners have racked up debts anywhere between $2 billion to $4 billion to finance the construction of their gargantuan facilities across North America, according to data compiled by CoinDesk and industry participants.

As the value of the miners’ output dramatically falls along with the price of bitcoin (BTC), they have to make tough decisions about how to survive – including selling off hard-earned coins and equipment.

“It was painful but necessary,” Alex Martini, CEO of mining hosting firm Blockfusion, told CoinDesk, regarding the selling of “millions” of dollars worth of bitcoin reserves to service the firm’s debt. Now Blockfusion has a cash reserve to last about six months, but “if the market doesn’t turn” the company “will be forced to do another round” of liquidations, he said.

Blockfusion is far from alone in this predicament. With the bitcoin price at its lowest levels since 2020, global processing power on the network, or hashrate, near all-time highs and energy prices climbing, miners’ profit margins are shrinking.

Older machine models are becoming unprofitable and turned off – the hashrate decreased by 11% between June 12 and June 27, data from Blockchain.com shows.

Miners once steadfast on their “hodl” strategy (holding bitcoin rather than selling it), are now being forced to liquidate their crypto holdings to pay for operating costs and loan installments.

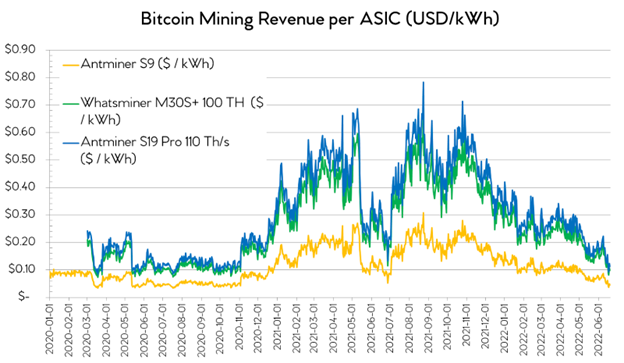

Bitcoin mining revenue in dollar-denominated terms per kilowatt hour (kWh) has more than halved since the start of the year, data compiled by Upstream Data President Steve Barbour shows. Using newer-generation machines such as the Antminer S19 Pros and Whatsminer M30S+ can make a big difference because they bring in double the revenue of older models like the Atminer S9, according to Barbour’s data.

The miners that use the latest machines and have low electricity prices – less than 6 cents per kilowatt hour, keeping their overall cost of mining a bitcoin below $10,000 – can still make ends meet and fulfill their loan obligations, said Brian Wright, Galaxy Digital’s vice president of mining.

Mining revenue for different mining rigs. (Steve Barbour/Upstream Data)

CoinShares investment analyst Alexander Schmidt told CoinDesk he thinks “the majority of listed miners” are still profitable even with the price of bitcoin around $20,000.

“Miners who don’t have leverage and run the new generation [machines], and there’s some of those in the United States, they’re probably still fine” in terms of profits, said Juri Bulovic, head of mining at Foundry Digital. Foundry is owned by CoinDesk’s parent company, Digital Currency Group.

Who racked up debt?

Adding debt into the equation paints a darker picture.

Publicly listed bitcoin miners have borrowed at least $2.16 billion, based on data compiled from a June 14 investor note from securities firm B. Riley Financial and including a $37 million loan disclosed by Bitfarms on June 17.

On the higher end, public and private miners have borrowed a total of $3 billion to $4 billion in loans backed by mining computers, estimated Chief Economist and Chief Operating Officer of mining firm Luxor Technologies, Ethan Vera.

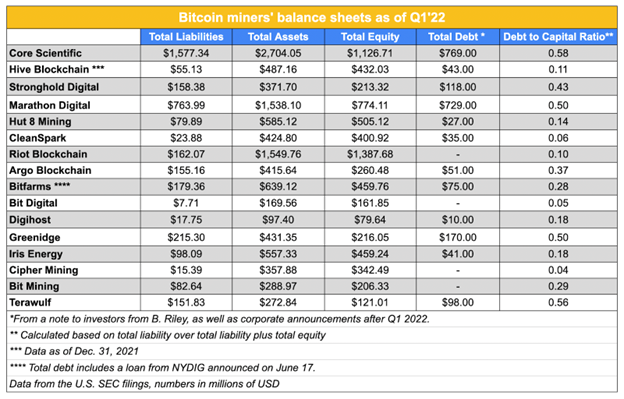

Core Scientific (CORZ) and Marathon Digital (MARA) are among the most highly leveraged miners based on their debt-to-capital ratios. However, their debt obligations are mostly secured promissory notes that don’t mature until 2024 and 2025, so they have time to pay off the loans.

The capital ratio is an indication of how high a company’s debt burden is relative to its equity. The higher the ratio, the bigger the risk.

A sample of miners’ assets and liabilities. (CoinDesk/Company filings)

Northern Data, a German hosting firm, has a debt-to-equity ratio of 1.84, according to data reported to the German stock exchange for 2020, the highest among miners surveyed by CoinDesk.

However the ratio doesn’t accurately depict the company’s finances today, Northern Data’s head of investor relations Jens-Philipp Briemle told CoinDesk via email. The miner acquired some of its creditors in 2021 paying off debts and at the same time managed to reduce a significant portion of its debt through the sale of a 300 megawatt site in Texas. The company has outstanding debt of EUR 20 million ($21 million) which it expects to pay off by August 2022, Briemle said.

Companies ideally don’t tap into their assets to pay off their debts, instead relying on their revenues to cover payments. Many miners are likely not bringing in enough revenue to pay off their monthly debt installments for these loans, regardless of what prices they bought machines at, considering common loan terms, said Bulovic.

For example, as of the end of the first quarter, Stronghold Digital Mining (SDIG) had outstanding borrowings of $70 million to pay off by the year end, but incurred a net loss of $30 million in the same quarter, according to a filing with the U.S. Securities and Exchange Commission (SEC). The miner did not respond to CoinDesk’s request for comment on this story.

Loans underwater

Miners that borrowed money to finance their expansion plans are now having to make tough decisions. Many “of those loans are underwater today” and borrowers need “significant revenues beyond the financing to remain current,” said Neil Van Huis, partner at BlockFills, which was one of the first firms to give out equipment financing loans to miners in 2020.

Equipment financing loans like the ones miners take out are “underwater” when the value of the loan exceeds the value of the underlying asset, such as bitcoin mining machines.

At the height of the market, when bitcoin was over $60,000, companies were purchasing miners at $90, $100 and even more per terahash, Bulovic said. That adds up to as much as $10,000 per machine. “The larger price tag means that the loan amount was higher. That means that the monthly payments are higher,” he said.

Firms that placed orders for mining rigs “at the height of the bull market for peak prices with a significant deposit,” are now “in a difficult spot to follow through,” said Jamie Leverton, CEO of Hut 8 Mining (HUT). “In due course, we’ll see some defaulted loans, unclaimed miners, and acquisition targets,” Leverton said.

Miners that were 100% financed, are less than two years old and are small without beneficial economics are likely to be the first ones to see defaults on the associated loans, said Van Huis.

Giving out bad credit

Miners’ difficulties in paying their installments engender risk for the overall ecosystem, as they leave lenders exposed to defaults. Hut 8 Mining’s Leverton said she expects miners to go into arrears. Miners have to prepare for the bear market during bull times, thinking about how to manage the cycles, treasuries and balance sheets, she said at CoinDesk’s Consensus 2022 conference in Austin, Texas, last month.

According to Van Huis, lenders BlockFi and NYDIG have given out “horrible credit” that miners will have a hard time repaying given current market conditions. These companies do not disclose how many mining loans sit on their balance sheets, so it’s hard to estimate how exposed they are.

After days of speculation over its finances – including a supposedly leaked balance sheet that purported to show the company suffered a net loss of $221 million amid 2021’s bear market – BlockFi announced it got a $250 million credit line from FTX. Many called it a bailout. The lender has not responded to CoinDesk’s requests for comment on this story.

Companies like “Celsius, BlockFi, specifically BlockFi and even NYDIG, when they were financing people at 75% to 80% LTV [loan to value] at $65 per terahash or higher, many of them were much higher towards $80 a terahash” have built “horrible credit for the industry because all of those loans are underwater today,” Van Huis said.

Loan-to-value ratios are used to assess the risk of a loan by comparing its value with that of the underlying collateralized asset. The higher the ratio, the higher the risk, which often translates into a higher interest rate.

Broadly speaking, in the past couple of years interest rates for equipment financing loans for bitcoin miners usually are in the double digits, between about 10% and 19%, publicly traded miners’ filings with the SEC show. (For comparison, even after recent increases, home mortgage rates in the U.S. run in the low to mid-single digits.)

An $80 price tag for a terahash of mining power looks high considering that application-specific integrated circuits (ASICs) are now selling for below $60/TH, according to data from Luxor’s Hashrate Index. This suggests that not only were the initial loans given out risky, but that the value of the underlying assets has significantly decreased as the value of ASICs has diminished.

“Some lenders took on more risk than others,” in terms of the protections that they have in place in cases of defaults and how they calculated LTV, Wright said. LTV can be calculated with the value of bitcoin or machines at the time the loan is given out, but a lender should consider what the actual liquidation price will be when the time comes, he explained.

BlockFi and NYDIG were giving out very large loans quite late in the cycle, said another industry insider who did not want to be named while commenting on other companies. This would mean that the price per terahash and therefore the monthly installments are higher. There are lenders in the market that are “very exposed” and “very worried,” the insider said.

BlockFi declined to answer a list of specific questions from CoinDesk. Chief Risk Officer Yuri Mushkin said the firm “runs a diversified lending business to the crypto ecosystem,” of which “mining-backed loans are only a portion.” Mushkin added, “These mining-backed loans are collateralized, and we follow the same prudent risk and underwriting practices that we implement across the rest of our institutional business.”

NYDIG didn’t respond to CoinDesk requests to comment on this story.

The New York-based lender signed off on a $70 million loan for Argo Blockchain in March and a $37 million credit line for Bitfarms on June 14. Along with the loan, Bitfarms said it was selling off 1,500 BTC. Just a week later, the miner said it had sold another BTC 1,500 to pay off its other debt from Galaxy.

Read more: Bitfarms Looks to Boost Liquidity With Sale of 1,500 Bitcoin, New Loan

TeraWulf also took on a $15 million loan in the form of a convertible promissory note on June 13.

If the “economics don’t change, it’s just a matter of time until some miners default” while at the same time “lenders have relatively little recourse” to “save themselves” because the value of collateral, usually mining machines or bitcoin, is dropping every day, the insider said.

Celsius recently halted withdrawals for customers without much explanation, triggering investigations from authorities in several U.S. states.

BlockFi, like Celsius, was working with funds raised from depositors, which means it has to pay them back, whereas NYDIG raised money through equity, so it will just take longer for it to recoup those funds, said Van Huis.

Only about 6% of Galaxy Digital’s $5.3 billion assets are related to mining, or $301 million, which would normally include loans receivable, according to a quarterly earnings report. The filing also details that the firm has prepaid $89.9 million in mining expenses and deposits, leaving about $211 million that could be the lender’s exposure to mining loans. A spokesperson declined to comment on the figures.

Hodl no more

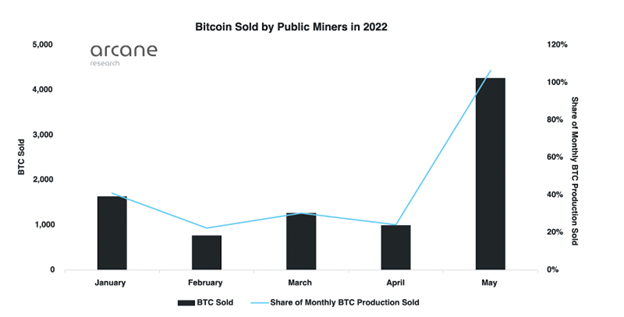

Miners have been selling bitcoin to exchanges at record paces. In May, bitcoin miners sold over 100% of their monthly production, compared to 30% between January and April, said Jaran Mellerud, senior researcher at Arcane Research.

Miners’ are selling bitcoins at record pace. (Arcane Research)

On-chain information platforms like CryptoQuant and CoinMetrics have noted record flows of coins from miners to exchanges over the past few weeks. This is not necessarily an indication of selling; it could mean that miners are staking their tokens or preparing to sell, Wright explained.

With tight liquidity, miners that pledged bitcoins they mined as collateral to get equipment loans might not be able to monetize them for anything other than paying off their debts. In these cases, the collateral is likely held by the lender, and will only be sold in the case of a margin call, Bulovic said.

This was the case for Blockfusion, which had a margin call at $29,000, according to the firm’s CEO. A margin call occurs when the value of a borrower’s collateral falls below a certain threshold, determined in agreement with the lender. In that case, the borrower has to come up with the funds to exceed that threshold, which sometimes means selling assets at unfavorable market prices–such as BTC below the $20,000 mark.

Blockfusion had to choose between posting more collateral or selling its bitcoin, Martini said, adding that most miners he knows “lost their collateral.”

At the same time, firms that raised money by taking on debt or diluted their stock by issuing more shares have restricted their ability to grow at this time because they have to either post additional collateral or liquidate their bitcoin holdings, said Matthew Schultz, executive chairman at CleanSpark, a bitcoin miner that bought existing contracts for 1,800 machines this month from another peer.

“We were presented with the same opportunity as everybody else,” Schultz said. CleanSpark had the chance to leverage bitcoin “for the benefit of a little bit of cash flow and then to see competition raised to the point that it becomes almost unrealistic,” he said. But the company avoided that, and has the second-lowest debt to capital ratio among surveyed miners.

To secure a $35 million loan from a venture capital funder earlier this year, CleanSpark instead collateralized its bitcoin mining rigs.

Machine free-for-all

Bitcoin miners that posted their machines as collateral are faced with a different set of problems. With miners looking to offload their machines for much-needed cash, the prices of ASICs have significantly dropped.

Ideally, miners would sell older machine models but there is no market for them at the moment because they are unprofitable, said CleanSpark’s Schultz, so they are “forced to sell newer equipment” or leverage their bitcoin.

Rack space is a limiting factor for those looking to buy up rigs.

If a firm that mines for its own account went bankrupt, it couldn’t mine at its site because it would be out of cash, so even if a lender wanted to take over the machines, they would have to find a hosting site to plug those machines in, Van Huis said. But all hosting sites are at maximum capacity, he added.

One U.S.-based mining hosting firm told CoinDesk that it has been getting an increasing number of calls from near-desperate miners looking to house cheaply bought rigs. But the host’s facilities are completely full so it can’t take any of the offers.

In an even more precarious spot are mining firms that took out loans secured with future orders, meaning contracts for machines that have yet to be delivered. These miners have to pay off rigs that aren’t making them any money at the moment.

Lenders and borrowers saddled with big loans “against purchase orders” are in a “tough position” because not only has the value of the machines significantly dropped, but the equipment is not even in the U.S. at the moment, Wright said.

“I don’t see how you can survive that,” Van Huis said.

Some miners may have to take on additional loans to buy rigs for which they already put down deposits.

“A sample set of public miners still owe $1.9 billion this year, for the ASIC purchases that they’ve committed to,” said Galaxy Digital’s head of mining, Amanda Fabiano, during a panel discussion at Consensus 2022.

Read more: Bear Market Could See Some Crypto Miners Turning to M&A for Survival

Regardless of what collateral miners used, its value has decreased in the past few months, Galaxy’s Wright said. “I haven’t actually seen a big difference between miners that pursued bitcoin-backed loans, as opposed to ASIC-backed loans,” he added.

Long-term consequences

Industry sources to whom CoinDesk spoke agreed the industry will consolidate in the coming months as weaker players are forced to offload assets.

This will not only bring opportunity for other players in the form of cheap ASICs, but will make it easier for those still participating to mine bitcoin.

“As less-efficient miners go offline, the lower network hashrate will directly benefit high efficiency machines with low shutdown prices,” Canaccord Genuity analyst Joseph Vafi wrote in a June 20 research note.

The difficulty of mining a bitcoin block and reaping the rewards automatically readjusts to keep the time required to around 10 minutes. The higher the network hashrate, the higher the difficulty.

The next difficulty adjustment is expected to make it easier to mine a block, as miners have dropped off the network.

Mining rig deliveries are still coming online, which will drive up the hashrate later in the year, said CoinShares analyst Alexander Schmidt.

At the same time, rising natural gas prices are putting additional pressure on margins for companies like Marathon Digital and Hut 8 that rely on this resource. “Miners powered 100% by renewables may benefit from lower competition,” Canaccord Genuity’s Vafi wrote.

Read more about

BTC$20,057.03

BTC$20,057.03

ETH$1,108.43

ETH$1,108.43

BNB$217.87

BNB$217.87

XRP$0.325625

XRP$0.325625

SOL$34.34

SOL$34.34

View All Prices

Sign up for The Node, our daily newsletter bringing you the biggest crypto news and ideas.