Bitcoin has emerged as an uncorrelated asset, but that hasn’t been such a good thing lately.

The largest cryptocurrency by market capitalization has trailed equities and other types of assets that have been surging, most recently amid encouraging early, second quarter earnings.

A Changing Narrative

Bitcoin’s narrative has frequently changed, depending on whom you spoke with and when you spoke with them.

Among other things, bitcoin has served as inflation hedge, providing protection against loose monetary policy, and high beta risk asset, generating surplus alpha relative to tech stocks. An investor’s interpretation of bitcoin’s current narrative may be driven more by philosophy than economics.

If you’ve invested in bitcoin because you view it as a means of portfolio diversification, with uncorrelated returns, then you’re likely pleased. If you’ve done so over the last three months as a means of generating returns, perhaps not so much.

While traditional financial indices have enjoyed recent success. Bitcoin has been mired in stagnant price action for the better part of the last three months.

The S&P 500, trading at 4567.46 is currently within 5% of its all-time high. Tech heavy Nasdaq is now trading within 15% of all-time highs. Meanwhile, the oft-watched Dow Jones Industrial Average (DJIA) is in the middle of its longest winning streak since 2017, rising 12 consecutive days, and within 4% of its all-time high.

Bitcoin sits at just 43% of its all-time high ($67,563), according to CoinDesk Indices data. Ether is trading at 38% of its prior maximum price.

While uncorrelated returns have been lauded as a benefit to owning digital assets, this is likely not what investors meant.

Crypto vs. TradFi Investors

Bitcoin’s decoupling from traditional financial assets certainly rings positive, but its lack of participation in recent market moves may be puzzling to some and could be attributed to differences between digital asset and traditional investors.

Bitcoin investors may view the current macro environment as fraught with risk, while Tradfi investors expect that the economy’s resilience in the face of interest rate tightening is a signal to add exposure.

The 90-day returns of 17%, 23%, and 11% for the S&P 500, Nasdaq and DJIA, compared to the 3% return for BTC over the same period indicate clearly where the current appetite for risk exists.

Oddly, BTC has trailed other digital assets over the identical period. XRP and Solana (SOL), in particular, have delivered stronger 90-day gains than has BTC and ETH.

An application of Julius de Kempanaer’s Relative Rotation Graphs illustrates bitcoin and ether’s weaker performance compared to peers, while using the S&P 500 as the central benchmark.

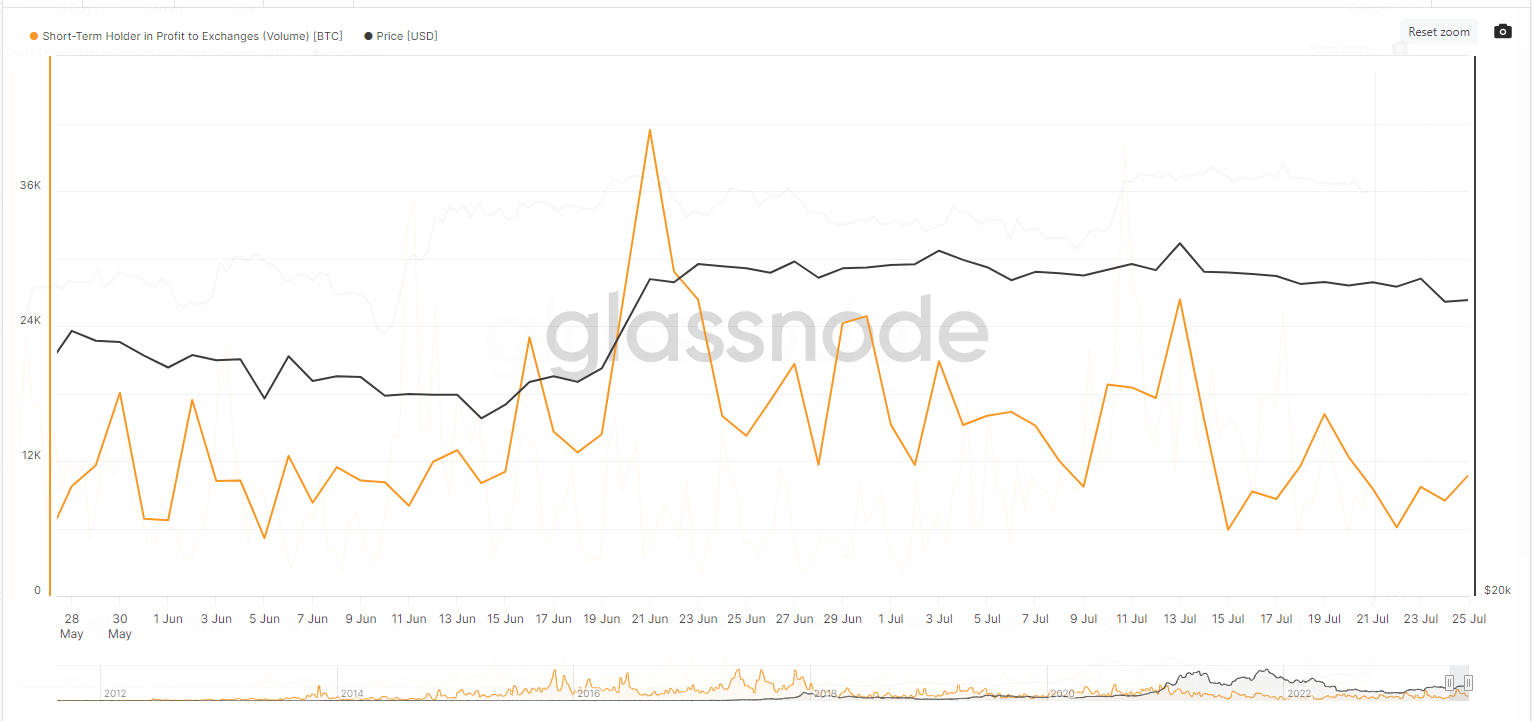

Still, much of BTC’s lack of performance may be attributable to short term traders. Per on-chain analytics firm Glassnode, the percentage of short term traders in profit has declined from 99% to 60% since July 13.

Another item worth monitoring is the transfer volume of coins from short term holders who actually are in profit. Transfer volumes to exchanges has increased 76% since July 22nd, implying that short term traders may be preparing to offload more bitcoin.

All told, bitcoin’s July has been eventful in many ways specific to headlines, but very few in regards to price. While its independence demonstrates a level of asset maturity, its displayed itself in a lack of price growth.

This article was written and edited by CoinDesk journalists with the sole purpose of informing the reader with accurate information. If you click on a link from Glassnode, CoinDesk may earn a commission. For more, see our Ethics Policy.