The Impact of Market Makers on Bitcoin’s Price Action

As Bitcoin’s (BTC) recovery rally gains momentum, the $90,000 mark has emerged as a pivotal level that could dictate future market dynamics. This projection is largely influenced by the current positioning of options market makers, who play a crucial role in the cryptocurrency market.

Market makers, often referred to as dealers or MMs, are integral to maintaining liquidity in the trading ecosystem. They take the opposite side of investors’ trades and strive to keep a market-neutral stance by hedging their positions across both spot and futures markets. Their profitability stems from the bid-ask spread, which is the difference between the prices at which they buy and sell an asset.

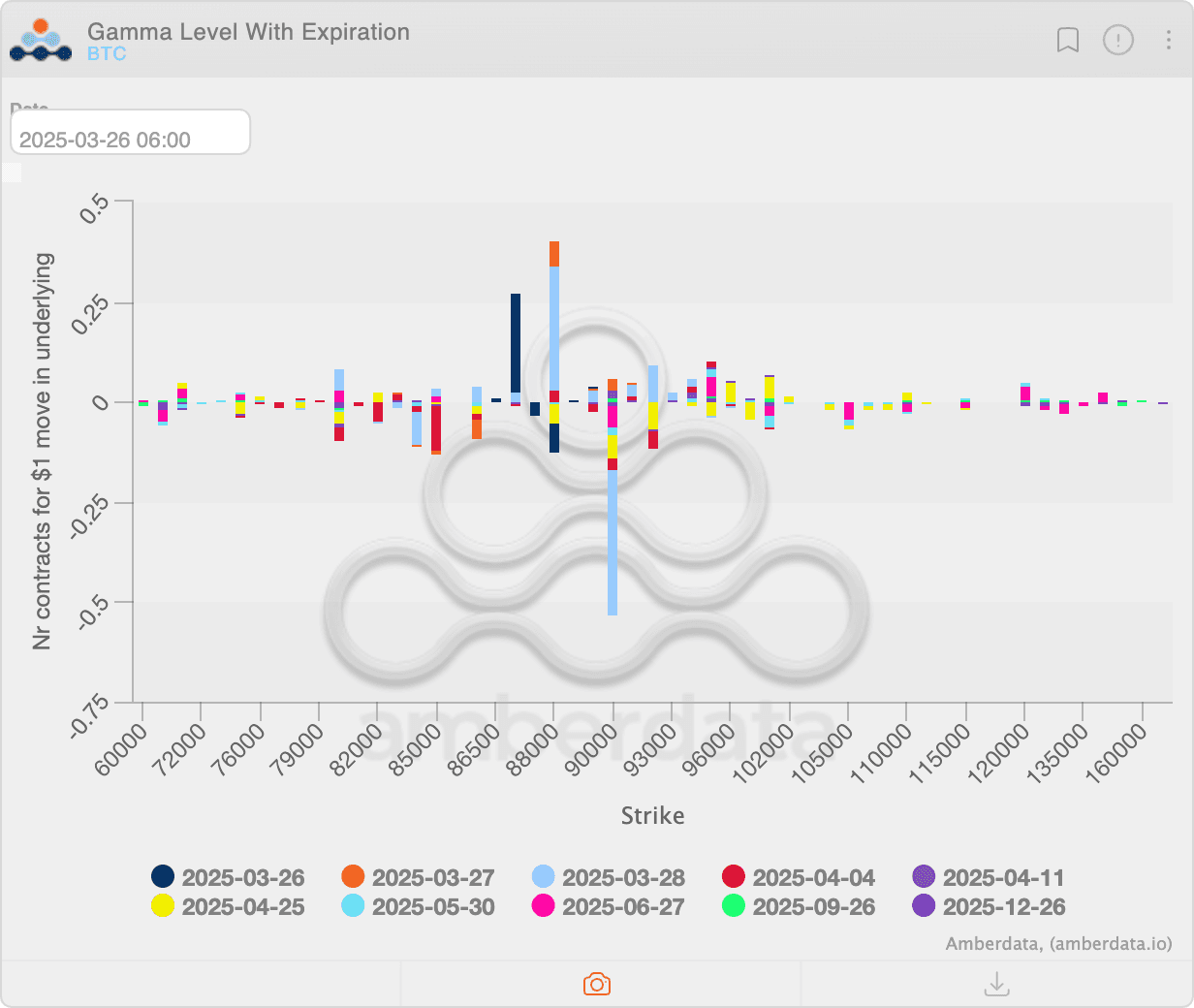

Recent data from Deribit regarding Bitcoin options, as tracked by Amberdata, indicates that market makers are currently “short gamma” at the striking price of $90,000. This means that as Bitcoin’s price approaches this level, market makers will be compelled to sell when the price drops and buy when it rises in order to maintain their market-neutral exposure. Such hedging activities are likely to contribute to increased market volatility.

“Given that negative gamma will continue to significantly influence the market even after the settlement, the hedging practices of market makers are expected to further amplify price fluctuations,” stated Griffin Ardern, the chief author of BloFin Academy and head of BloFin Research and Options, in an interview with CoinDesk. “However, the likelihood of upward price movement appears to be greater at this point.”

Gamma denotes the rate of change in delta, which measures an option’s price sensitivity to fluctuations in the underlying asset’s price. Being short gamma means holding a short position in options, which can lead to substantial financial losses, particularly in volatile market conditions. Consequently, when market makers are in a short gamma position, they must align their trades with market movements to keep their portfolio balanced.

Conversely, the scenario changes when market makers are long gamma. Toward the end of the previous year, they were long gamma at both the $90,000 and $100,000 levels, resulting in a consolidation phase between these price points.

Examining the dealer gamma distribution in Deribit’s BTC options reveals that the $90,000 strike will likely maintain the most negative delta following the quarterly settlement scheduled for this Friday. This indicates that the hedging activities of dealers could further influence price swings around the $90,000 threshold.

According to Ardern, the dealer gamma profile of BTC after Friday’s expiration is expected to resemble that of the gold-backed PAXG token. “Once the effects of the options set to expire are accounted for, PAXG exhibits a gamma exposure distribution similar to that of BTC. The price tends to find support following significant declines and faces resistance during considerable upward movements, resulting in a broad range of price fluctuations,” he explained.