Crypto lender Celsius has half a million creditors owed more than $5 billion, attorneys for the company said during its first bankruptcy hearing Monday.

News of Celsius’ liquidity crisis broke on June 12, when the company announced it was pausing all customer withdrawals, citing “extreme market conditions.” The company formally filed for Chapter 11 bankruptcy protection in the Southern District of New York (SDNY) last week.

The situation at Celsius is not unique: the lender is one of several that have been hit hard by the Terra/LUNA crash, the insolvency of Three Arrows Capital and the ongoing market downturn.

Struggling crypto lender BlockFi received a $250 million bailout from crypto exchange FTX in order to fulfill customer withdrawal requests – and could be acquired by FTX for as little as $240 million more. Less than three weeks after Celsius halted its withdrawals, Voyager Digital followed suit, before it also filed for Chapter 11 bankruptcy in SDNY on July 6.

Court filings paint a concerning picture for Celsius’ creditors, most of whom are average retail investors. The company has an enormous $1.2 billion hole in its balance sheet (at least) – and retail depositors who held their crypto in Celsius accounts will likely be the last to get paid back.

Chapter 11 bankruptcy, also called a “reorganization bankruptcy,” pauses any attempts at civil litigation from creditors, and allows the company time to get its finances in order to repay its debts.

Breaking down Celsius’ bad debt

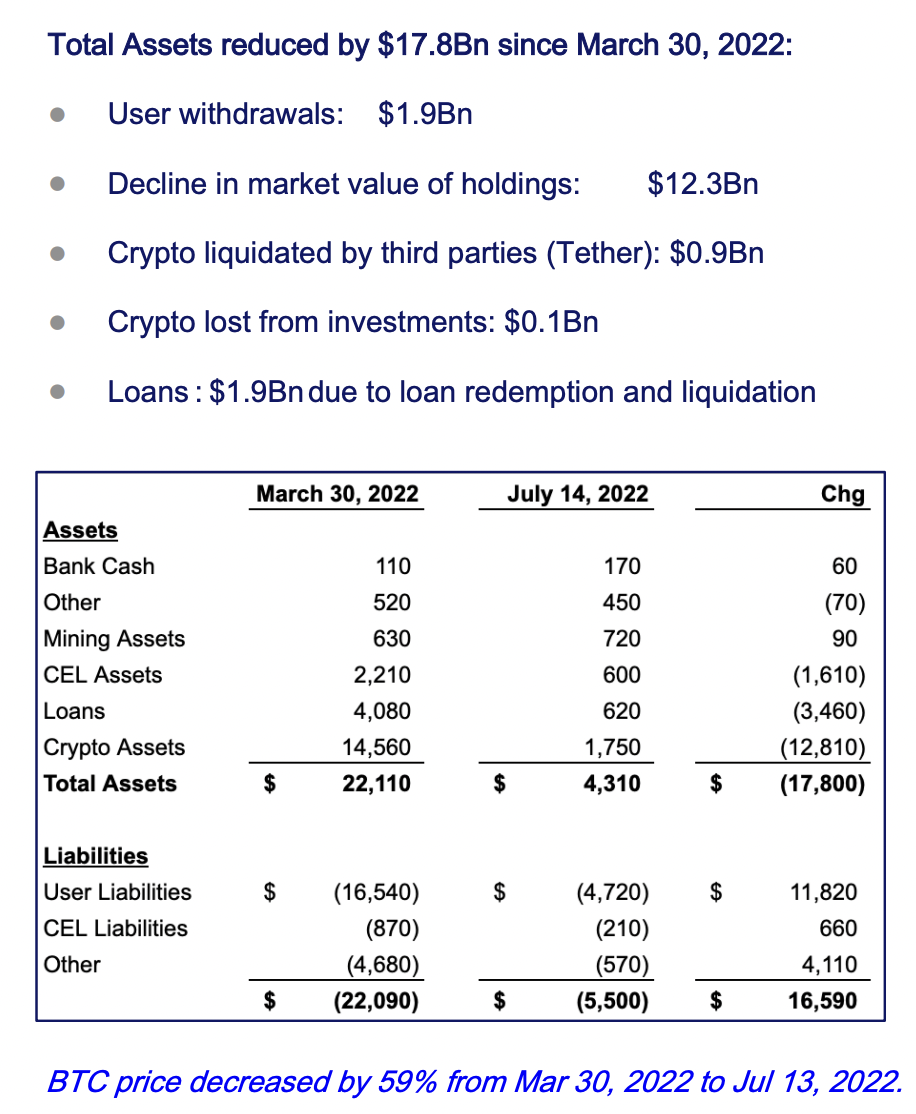

Documents filed to the Southern District by the company’s law firm Kirkland & Ellis show that Celsius is deeply insolvent.

Read more: Looking at the Claims Celsius Operated Like a Ponzi

Leading up to declaring bankruptcy, Celsius saw its digital asset holdings dwindle to a mere $1.7 billion as of July 14, down from $14.6 billion since the end of March. The documents also show that Celsius owes $4.7 billion to its customers, almost three times what it holds in digital assets.

Celsius also holds $170 million in cash held in a bank, but the rest of the assets are tied up in mining equipment ($720 million), outstanding loans ($620 million) and other assets ($450 million). The documents also somehow account for $600 million in the platform’s CEL token, a much higher value than the total market capitalization of the coin. (The CEL token faces regulatory scrutiny by the Securities and Exchange Commission.)

The firms claimed that most of the drop was due to the collapse in crypto prices, shrinking its assets by $12.3 billion.

The rest of the losses added up as:

-

Users withdrew $1.9 billion from deposits up until June 12, the date when the company suspended withdrawals.

-

Loan redemptions and liquidations reduced the firm’s assets by another $1.9 billion.

-

Tether, the issuer of the largest stablecoin USDT in the market and also an investor in Celsius, set back the firm by an additional $900 million when it liquidated a loan to Celsius. (Tether issued a statement about the liquidation.)

-

And the firm also lost $100 million from investments.

A breakdown of Celsius’ asset losses in court filings. (Kirkland & Ellis)

Another document filed for the court listed the crypto lender’s “unanticipated losses to the business.”

Namely, the Ethereum staking platform StakeHound lost access to 35,000 ETH ($50 million at current prices) that Celsius deposited on the platform to earn a yield “due to an alleged error by StakeHound’s third-party crypto custody provider Fireblocks.”

StakeHound and Fireblocks are currently involved in litigation over the matter.

A private lender, reportedly the Indianapolis-based lending platform EquitiesFirst, failed to return the collateral of a loan Celsius paid off and owes $439 million to Celsius.

Celsius admitted it also lost about $15.8 million in Terra’s collapse, but the “widespread and completely misleading Twitter and social media commentary,” as the company’s legal advisor said during today’s hearing, prompted a run on its deposits in the first place.

A mining Hail Mary

Monday’s hearing – as well as a host of court documents, including a 61-page declaration from CEO Alex Mashinsky – indicate that much of Celsius’ plan to recoup its losses depends heavily on the projected future profits of its half-finished, wholly-owned mining subsidiary, Celsius Mining.

However, that mining subsidiary is also a debtor. Lawyers for Celsius asked the court on Monday to approve over $5 million in spending to finish the construction of the mining center in Texas (which Celsius’ attorneys said would take approximately two more months), as well as pay duties on mining rigs “currently sitting with the customs authorities.”

Though Judge Martin Glenn, chief judge of the U.S. Bankruptcy Court in the Southern District of New York, approved the request on an interim basis, the U.S. Trustee – the arm of the Department of Justice that oversees administration of bankruptcy cases– will ultimately hold the purse strings.

At Monday’s hearing, Shara Cornell, an attorney with the U.S. Trustee Program, voiced her concerns about the viability of Celsius’ mining operation.

“There’s one mining company that I don’t believe is currently operable, but has caused the debtor a considerable amount of money. I’m not clear if construction may or may not be the best avenue for the debtor at this time,” Cornell told the court. “Why not just consider liquidating it and move on?”

Celsius’ attorneys pushed back, claiming that Celsius’ operation already included more than 43,000 mining rigs, with plans to reach 112,000 mining rigs “sometime in Q2 of 2023.”

Pat Nash, Celsius’ lead attorney, told the court that the mining subsidiary was mining approximately 14.2 bitcoins per day – and expected to mine 10,100 bitcoins in 2022.

“If everything goes well, in 2023 we hope and expect to be in a position to mine approximately 15,000 bitcoin a day,” Nash told the court (Nash presumably meant 15,000 bitcoins in the entire year, as only roughly 900 total bitcoins can currently be mined per day).

Retail customers will suffer

Even if Celsius’ promises to mine 10,100 this year are accurate (something that is difficult to independently verify), at current market prices that would yield approximately $225 million – only a fraction of what is needed to make Celsius’ solvent.

When Celsius begins to make good on its $5.5 billion in liabilities – $4.7 billion of which represents customer holdings – its customers will almost certainly be last to get their money back. And by then, there might not be any money left.

Read more: Celsius Bankruptcy Filings Hint Retail Customers Will Bear Brunt of Its Failure

“Celsius has set the stage for conflict between its customers and its sophisticated institutional investors,” Daniel Gwen, a business restructuring associate at New York-based law firm Ropes & Gray told CoinDesk.

“In particular, Celsius has pointed out in its pleadings that customers transferred ownership of crypto assets to Celsius, making those customers unsecured creditors. This detail may undercut customer expectations, who thought they were depositing their assets into a construct similar to a traditional bank,” Gwen added.

Nash told the court on Monday that Celsius has approximately 500,000 depositors, 300,000 of which have more than $100 worth of crypto in their accounts.

Celsius’ attorneys asked the judge to redact names and other personally-identifying information from Celsius’ creditor matrix and other documents, citing Celsius’ employees and corporate creditors’ fear for their personal safety.

“These cases have generated a lot of press and social media commentary. Certain employees have been receiving death threats and hate mail,” an attorney for Celsius told the court. “We received certain communications from scheduled corporate creditors stating that corporate principals have been receiving death threats and hate mail as well.”

Next steps for Celsius

The second hearing in Celsius’ bankruptcy proceedings will be held remotely on the morning of August 10.

The U.S. Trustee is currently in the process of forming and appointing a committee of creditors. These committees are typically made up of the seven largest unsecured creditors of the debtor, and help oversee the bankruptcy proceedings, investigate the debtor’s conduct and business operations, and help the court formulate a reorganization plan for the company’s debt.