The Takeaway:

-

Celsius Network, an interest-earning yield platform, has frozen withdrawals after using a myriad of failed decentralized finance (DeFi) strategies.

-

It suffered a series of severe losses including over 38,000 ETH in a blunder related to Stakehound, followed by a $22 million loss in connection with the Badger DAO hack.

-

Customers now fear they will never be able to access funds that are locked on Celsius.

-

Already reeling from last month’s LUNA collapse, the cryptocurrency market has shed $180 billion off its market cap in the wake of Celsius’ announcement, and major exchanges have announced job cuts.

If the collapse of LUNA was cryptocurrency’s Bear Stearns moment, Celsius Network threatens to become the industry’s Lehman Brothers: the failure that exacerbates a market crisis.

Celsius, which resembles a bank while touting itself as a democratized interest income and lending platform, is rumored to be insolvent following a freeze on withdrawals over the weekend. Founded in 2018, Celsius had more than $8 billion lent out to clients and $12 billion in assets under management by May of this year, according to the company.

In the wake of the withdrawal freeze, Coinbase, BlockFi and Crypto.com have announced job cuts, while insolvency rumors are also beginning to emerge from crypto hedge fund Three Arrows Capital.

Aside from the short-term implications, overall trust in the crypto industry is falling to new lows following a six-week period that has seen $60 billion evaporate in the LUNA crisis followed by the troubles at Celsius.

CoinDesk has received multiple reports from Celsius users over the past few weeks, some of whom are worried about losing their homes after being liquidated on millions of dollars of loans backed by the company’s cratering CEL token. CEO Alex Mashinsky often touted these loans as a “megadeal” during livestreams.

“Of course, now with the deteriorating economy I am very worried that I could lose my home if the housing market crashed,” said one user.

“CEL was my backstop, my safety net. I did have other crypto but it all blew up as I tried to prop up my loans,” said the person, who asked to remain anonymous but provided CoinDesk with screenshots showing liquidated loans.

Despite numerous attempts to contact Celsius and Mashinsky, CoinDesk has not received a formal response, although Mashinsky tweeted Wednesday that he and his team are “working non-stop” to resolve the issues. The company has reportedly hired restructuring attorneys.

Using DeFi to generate a yield

While the decision to halt withdrawals and transfers may come as a surprise to investors, the issues at Celsius and its ambitious attempt to generate high yields have been brewing for quite some time.

Read more: What Crypto Lender Celsius Isn’t Telling Its Depositors (2020)

On-chain data suggests that over the past few months, Celsius has been using a multitude of DeFi protocols including Terra’s Anchor and Ethereum stalwarts Lido and Curve in order to leverage client funds to pay out 17% APY in yields. Nansen, a blockchain analytics provider, identified the wallets making these trades as connected to Celsius.

Generating yield this way would be a shift in strategy. Two years ago, Celsius was lending to human traders and it controlled the risk by requiring collateral from these borrowers.

“There’s a lot of confusion about where yield comes from,” Mashinsky said during a video in 2020. “Celsius generates a certain amount of profit by lending assets, similar to what banks do. We lend them out on a short-term basis. These are not loans. We lend financial assets to players that can transact and generate income for themselves through arbitrage, market making or shorting certain stocks or digital assets.”

“We are the equivalent to [securities lending] in the digital world,” Mashinsky said, referring to a longstanding Wall Street practice.

He framed this as a more conservative strategy than DeFi, in which one lends not to a person or company but to a pool of assets controlled by code, albeit with ample collateral as well.

“We keep going back and comparing apples and oranges when we talk about, for example, stocks or bonds that pay dividends versus DeFi versus, for example, doing [yield] farming or doing all kinds of high-risk things,” Mashinsky said in 2020.

But since early 2021, when DeFi became more attractive, Celsius rapidly became more brazen in its attempts to generate high yields.

Lending to DeFi has a different risk profile than Celsius’ previous model.

“On the one hand, there is smart contract risk, there is protocol risk,” said Alex Thorn, head of firmwide research at Galaxy Digital, a crypto investment bank. “Also, lending in DeFi exposes you significantly to volatile market moves, whereas lending to a creditworthy institutional borrower is significantly different. [The risk] isn’t the same as relying on crypto market prices to sustain or grow.”

In this regard, “putting customer assets in DeFi markets is significantly riskier than lending on a secured basis to institutional counterparties.”

One possible advantage of Celsius’ pivot, however, at least for outsiders, is that DeFi is far more transparent.

“All of the crypto traders are watching these positions to see when Celsius will get liquidated,” Thorn said. “This is something that is not possible in traditional finance and certainly not in private debt arrangements.”

Last month, the Terra blockchain’s algorithmic stablecoin UST collapsed; this caused total value locked (TVL) in the ecosystem’s Anchor Protocol to drop from $14 billion to less than $5 million, according to data provider DeFi Llama. On-chain data, first reported by The Block, suggested that Celsius hastily pulled $500 million out of the Anchor Protocol during the chaos.

However, Mashinsky claimed that “Celsius Network did not have any meaningful exposure to the depeg” in spite of speculation to the contrary.

DeFi disasters

In June 2021, Ethereum staking service Stakehound disclosed that it had “misplaced” private keys for over 38,000 ETH. On-chain data provided by Nansen suggests that Celsius lost at least 35,000 ETH as a result, being left with the now-worthless Stakehound ETH tokens.

Celsius did not inform customers of the loss; instead, CEO Mashinsky was seen on a livestream shortly after holding a skateboard with the words “hodl,” crypto slang for “don’t sell in a panic.”

“The way to become a millionaire or a whale is to hodl,” Mashinsky said.

This was the first of many unfortunate events that hurt Celsius’ ability to deal with market downturns. Celsius also lost $22 million after it mistakenly forfeited restitution payments from the Badger DAO hack, according to a blockchain analysis by DirtyBubbleMedia.

On June 10, blockchain sleuths found that Celsius has meaningful exposure to Staked ether (stETH), which has depegged from ether at a ratio of 0.93:1 this week.

Not to be confused with Stakehound’s product, Staked ether is a product released by Lido Finance. It is given to users that stake ether for validator purposes ahead of the upcoming Ethereum Merge, when the blockchain shifts to a proof-of-stake consensus model.

Each stETH token is claimable for 1 ETH following the Merge. However, the lack of liquidity and demand, coupled with the potential of the Merge being delayed, has seen stETH lose relative value.

Several asset managers including Alameda and Amber Group have unloaded significant amounts in recent weeks, with Amber withdrawing $128 million from the Curve pool to a wallet and sending most of that to the FTX exchange, possibly for cashing out.

On June 7, Celsius had liabilities of more than 1 million ETH, according to an analysis by crypto investor Brad Mills. The Celsius liquid reserves amounted to just 268,000 ETH, with a further 288,000 inaccessible until after the Merge is completed. If users began to request ether withdrawals beyond Celsius’ liquid reserves, it would be forced to liquidate its stETH holdings at a 7% discount, not including the slippage that would occur due to a lack of liquidity, wrote Twitter user @Crypto_Joe10 in a highly detailed thread.

Mounting pressure forced Celsius’ hand

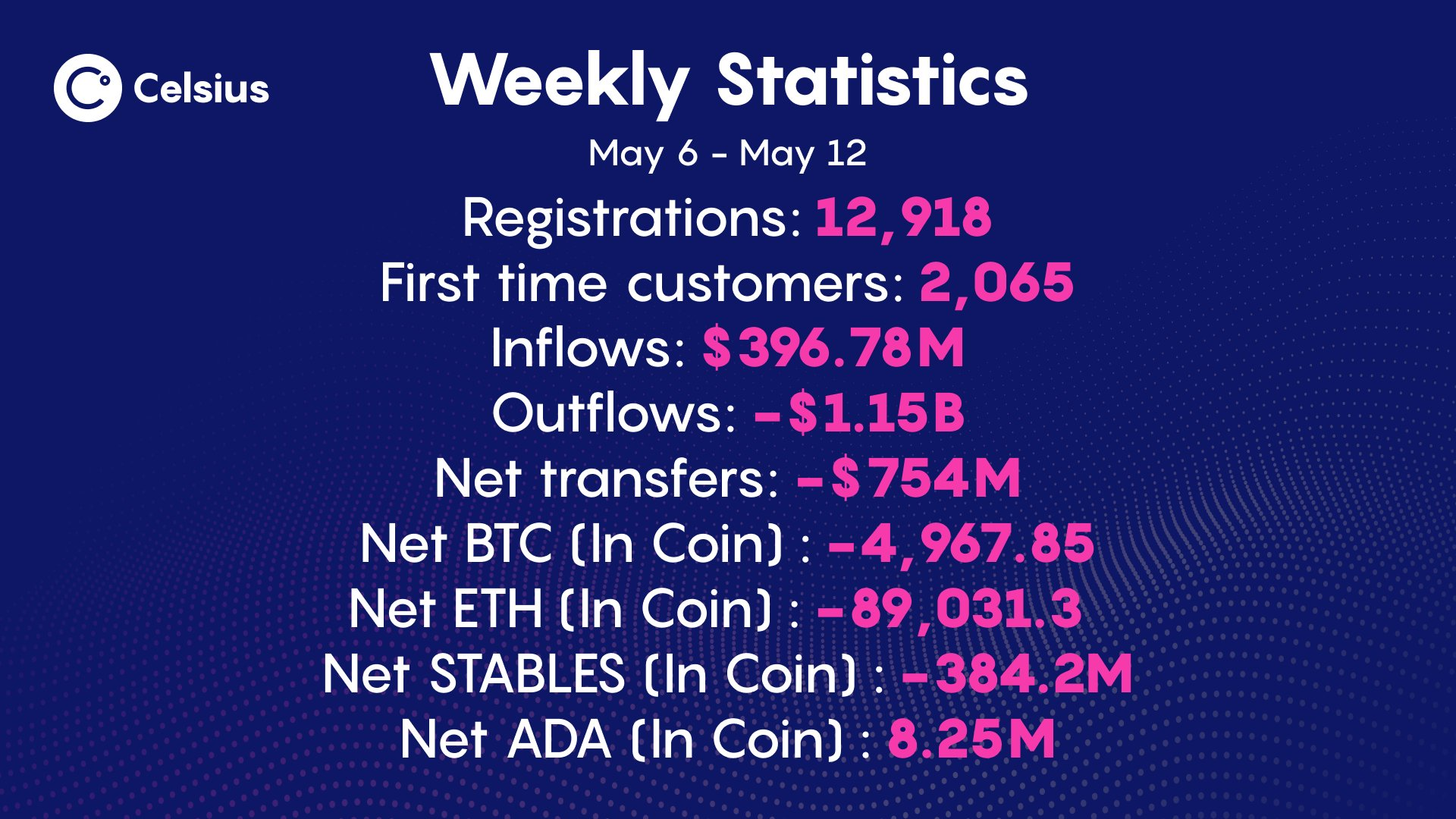

Every week Celsius hosts an Ask Me Anything (AMA) on its YouTube channel with the stated aim of being transparent with users. Every week since early May, the time of the Terra implosion, platform outflows have exceeded inflows; in the first week of May, outflows topped $1 billion.

Celsius outflows in May (Celsius/Twitter)

With investors pulling liquidity out faster than others were willing to risk putting it in, Celsius found itself in a difficult position as it had to expand revenue streams in order to continue paying out its ambitious yield to customers.

“I think they were totally unprepared for the market to tank,” another verified user told CoinDesk. “It seems like they had a number of highly complex leveraged long positions.”

“I initially put my stack into Celsius because they were FCA-approved,” the person added, referring to the company’s inclusion in a temporary registration regime of the U.K. Financial Conduct Authority. (Celsius later withdrew its application for full authorization and shuttered U.K. operations.)

“I had the (incorrect) understanding that my deposits were covered by the U.K. deposit protection scheme,” despite the regulator’s caveat that being on the provisional list “does not mean that the FCA has assessed [a company] as fit and proper.”

“I only ever received about 3%-5% APR yield on my bitcoin,” the user went on. “This did not seem unreasonable, given Celsius’ stated business model. However, once Celsius paused all withdrawals on their accounts, I looked closer. I would describe their use of DeFi protocols as gambling with customers’ money.”

Cory Klippsten, CEO of Swan Bitcoin, a platform for buying and storing the original cryptocurrency, is an outspoken critic of Celsius. He has been watching the company since its initial coin offering (ICO) in 2018.

“The red flags came when Alex Mashinsky’s claims didn’t match up with his background,” Kippsten told CoinDesk. “He didn’t have $3 billion in exits and he didn’t have the most successful IPO of 2004.”

Another warning sign came when custodian Prime Trust dropped the firm, citing Celsius’ habit of rehypothecating assets, or pledging borrowers’ collateral as security for its own borrowings.

Read more: Custodian Prime Trust Cuts Ties With Crypto Lender Celsius (2021)

The reports of Celsius yanking $500 million from Anchor before LUNA unraveled led Klippsten to further question the risks Celsius was taking with client funds. “‘What are they doing?’ I thought.”

Looking forward

The route ahead for Celsius and its investors remains uncertain; while the company has remained relatively quiet on social media, on-chain data shows that it is actively juggling funds and loans with market makers and DeFi protocols to ensure it isn’t liquidated on leveraged positions. On June 13 it sold some of its stETH position before adding collateral to a loan on Maker that was nearing liquidation.

More headwinds may lie ahead for Celsius, which according to a Radio Canada report may find itself in hot water with regulators after offering unregulated lending services to citizens. Last year it was issued a cease-and-desist order in Kentucky while regulatory pressure also mounted in Alabama, New Jersey and Texas. On Thursday, Texas and four other US states announced that investigations were underway into Celsius’ move to freeze withdrawals.

The company neatened up its risk disclosures in recent weeks amid regulatory uncertainty. It also restricted access to its Earn product to accredited investors.

In the official update outlining its reasoning behind halting activity on the platform, Celsius said the step was necessary to ensure that it can honor its withdrawal obligations.

“Our ultimate objective is stabilizing liquidity and restoring withdrawals, transfers and swaps (crypto-to-crypto trades) between accounts as quickly as possible. There is a lot of work ahead as we consider various options, this process will take time,” it added.

With the Celsius brand in tatters and the CEL token now trading at 60 cents, 93% lower than its all-time high of $8 one year ago, the company has the daunting task of regaining a reputation built during the previous bull market.

The second user that gave CoinDesk a verified account of their Celsius experience, said: “I hope to get my bitcoin back from Celsius. I’ve written to them saying I’d be happy to just receive my deposited bitcoin less any interest it’s accrued over the years. I expect to get back nothing, so I hope at least for an apology.”

Read more about

Save a Seat Now

BTC$20,941.21

BTC$20,941.21

ETH$1,102.80

ETH$1,102.80

BNB$215.77

BNB$215.77

XRP$0.315119

XRP$0.315119

BUSD$1.00

BUSD$1.00

View All Prices

Sign up for Market Wrap, our daily newsletter explaining what happened today in crypto markets – and why.