Two weeks ago, I thought the biggest story for the week of Nov. 8 would be the U.S. midterm election. Control of both the House and the Senate were up for grabs, with the future of crypto legislation at stake. All of that’s still true, but FTX collapsed in incredible and rapid fashion, with the effects reverberating throughout the world, and that’s really taken precedence in both crypto interest and national attention right now.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

FTX Went Mainstream

The narrative

FTX filed for bankruptcy last week, in what appears to be the most chaotic way possible.

Why it matters

The vibe has shifted. When Terra collapsed it was because it was a quirky crypto experiment that was obviously not going to succeed and thank goodness its effects were just limited to other crypto companies. Celsius and Voyager filed for bankruptcy and, wow wait, what were these companies doing with customer funds? Three Arrows fell apart – but again, hey it’s a crypto hedge fund or something, the broader world isn’t going to care.

FTX is something new. Partly because of how ridiculously this whole thing fell apart, partly because of just how insane some of what’s been reported seems and largely because of how much FTX tried to become a part of the broader world, everyone is paying attention. That’s going to lead to some interesting outcomes in the fallout.

Breaking it down

I’m going to quickly recap what happened. For those of you who have not closed Twitter in the last 170 hours or so, feel free to jump down to the next subheading.

On Nov. 2, my colleague Ian Allison published a report revealing that much of the balance sheet for Alameda Research, a quantitative trading firm, was composed of a large amount of the FTT token, which is issued by the cryptocurrency exchange FTX. Alameda and FTX share the same founder and ownership, so this immediately raised some questions about the figures these companies were reporting and in particular, whether this meant that either company had all the funds they claimed.

Sam Bankman-Fried, the founder in question, took to Twitter to reassure investors that everything was fine. A few days later, he and Binance’s Changpeng Zhao announced Binance would acquire FTX. Then CZ pulled out. But FTX US was still fine, Bankman-Fried said.

And then on Friday, FTX Group filed for bankruptcy, including FTX US, Alameda Research and, bizarrely, a bunch of companies that weren’t actually under the FTX umbrella and were quite surprised to discover they were listed. A leaked Excel spreadsheet reported by the Financial Times suggested FTX had less than $1 billion in assets, against around $9 billion in liabilities (and was written in such a way that Bloomberg’s Matt Levine possibly went insane).

The bankruptcy filing was chaotic, to say the least. At the time of writing, we still don’t even have a full bankruptcy document. We just have the top sheet where FTX says loosely how many creditors it has (over 100,000) and checks off ranges for its assets and liabilities ($10-$50 billion for both).

*Editor’s note: FTX, Alameda and the various companies finally began filing more information late Monday night. Click here for more.

The sheer insanity of what happened was perhaps driven home late Friday night, when after everything else, the exchange was hacked (or “hacked”).

This story has naturally drawn mainstream attention from around the world. My friends have asked about it. My parents have asked about it. My parents’ friends have asked about it.

And that is just one of the reasons why it’s worth exploring just how deeply entrenched FTX became over the past two years or so.

Sheer scale

It would be difficult to overstate the reach FTX had. Bankman-Fried was a major political donor over the past two years. He donated millions to the winning campaign of now-President Joe Biden in 2020. He donated to primary candidates and lawmakers from both parties this year.

Some of these lawmakers are already starting to announce they’ll donate the funds tied to Bankman-Fried. CoinDesk continues to reach out to the rest.

GMI PAC, a political group backed by Bankman-Fried, saw 19 candidates it backed win.

Within the ordinary course of business, Bankman-Fried was testifying on crypto legislation before Congress and proposing novel ways of settling derivatives trades to the Commodity Futures Trading Commission.

The chair of the CFTC expressed on multiple occasions how interesting the proposal was.

Bankman-Fried took photos with lawmakers and regulators.

There’s also a conspiracy theory that FTX was a Democratic Party psyop designed to funnel crypto investors’ money to the party as part of a broader push to kill crypto, or that Ukraine funneled money to the Democratic Party by way of FTX. Sometimes this theory also trades in antisemitic tropes. This is very dumb.

For one thing, Bankman-Fried didn’t only donate to Democrats, though he was a major party donor. For another, he donated a lot to primary candidates who didn’t win. Also, it’s probably worth noting that FTX Digital Markets Co-CEO Ryan Salame donated heavily to Republicans.

I’ll trust that if you’re reading this newsletter, I won’t need to explain that antisemitism is bad (and also, for what it’s worth, not even accurate).

Beyond that, though, FTX really did sponsor or partner with all sorts of things. There was FTX Arena, the home of the Miami HEAT basketball team. There was Major League Baseball, where every referee had an FTX patch on their jerseys. There was the Ukrainian Ministry of Finance, which FTX helped funnel donations to. A Formula 1 team. The Golden State Warriors. The World Economic Forum. The University of California – Berkeley’s entire athletic department. Not one, but two different esports organizations. If you went to Boston, you saw FTX signs on the street. If you went to the Bahamas, you could attend multiple conferences with FTX branding. The company really was everywhere. That’s a lot of normies who saw the name or logo somewhere, even if they didn’t follow the crypto sector all that closely.

FTX worked with companies to issue Visa debit cards, Bankman-Fried had a sizeable stake in Robinhood and former world leaders and luminaries took the stage with him.

And this doesn’t even get into all the venture capital firms and others who invested in FTX.

A lot of these groups are now starting to cut ties with FTX. Unlike the Nationals’ Terra deal, it does not appear that many of these sponsorships were prepaid, meaning those groups now have to find new sponsors. And as for the rest of these companies or groups, I’d imagine they’re going to be cutting ties and and the non-crypto folks are going to be asking a) how did a company with apparently no internal controls come to occupy such a large space in the world and b) what will regulators do to prevent this from happening again.

The backlash is going to be severe.

I spoke to several lawyers and D.C. insiders about the situation last week as things unfolded. One thing that’s clear: lawmakers are paying attention. There’s talk of hearings, potentially before the end of this year, according to Ron Hammond at the Blockchain Association, an industry lobbyist group.

I wrote a bit about the different ways that backlash could evolve for CoinDesk on Monday.

One possible reaction is that regulators will become more proactive about how they oversee crypto, rather than reactive. This is the fourth major failure this year – Luna, Celsius, Three Arrows and now FTX. Is this going to spur actual global coordination around crypto regulation? Or even just unilateral action from entities like the Securities and Exchange Commission?

It’s not immediately clear to me what U.S. regulators could have done about FTX specifically, given it headquartered in the Bahamas.

We haven’t heard anything specific on this yet, and I suspect it may take a while before we will. But the amount of attention FTX is getting makes me suspect that there will be pressure from lawmakers to act swiftly, rather than wait for the next shoe to drop.

And as Ken White, a former federal prosecutor and a partner at the Brown White & Osborn law firm, told me, this is the kind of “splashy” case that investigators would want to prosecute.

“There’s tons of fraud and securities fraud out there and the Feds can’t go after it all. The things they go after tend to be big in numbers or splashy or somehow sexy and high profile,” he said. “This is all those things. A huge amount of money, it’s very public … it involves exciting new technology and new ideas and all that. It’s exactly the type of case that the Feds would invest resources into going after.”

On the other hand, the financial shock appears to so far be contained within the crypto ecosystem. One issue several regulators had warned about pre-FTX was the possible contagion risk posed by crypto becoming a part of the broader financial system. So far, that hasn’t happened yet. That could blunt the regulatory response somewhat.

On another note, there is no way to succinctly sum up the sheer amount of coverage CoinDesk has published over the past week and change. Click here for a list of all our recent stories.

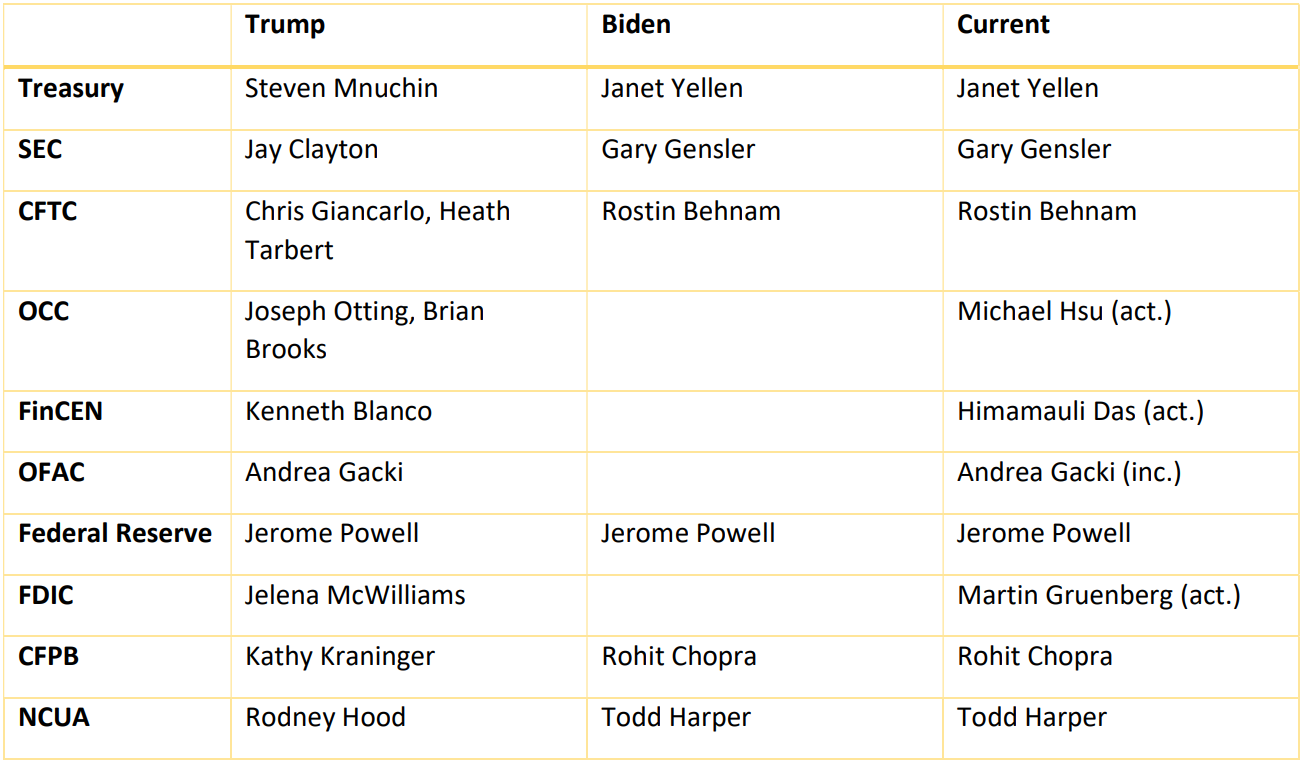

Biden’s rule

Changing of the guard

Key: (nom.) = nominee, (rum.) = rumored, (act.) = acting, (inc.) = incumbent (no replacement anticipated)

Fresh off the news that Democrats would retain control of the Senate for the next two years, U.S. President Joe Biden has nominated Acting Federal Deposit Insurance Corporation Chair Martin Gruenberg to a full term helming the agency. Senate Banking Committee Chair Sherrod Brown (D-Ohio) praised the move. House Financial Services Ranking Member Patrick McHenry (R-N.C.) called it a partisan section. And the Conference for State Bank Supervisors lamented the lack of state bank supervisors on the FDIC.

Outside CoinDesk:

-

(The New York Times) Former FTX CEO Sam Bankman-Fried is still giving interviews. He spoke to the Times about recent events.

-

(The Washington Post) There was a tweet last week from a verified account claiming to be pharmaceutical giant Eli Lilly. The tweet said that insulin would now be free. The actual Eli Lilly was surprised and unamused. It’s now canceling its Twitter ad buys.

-

(HSE University) Longtime readers will know I’m a nut for all things LEGO. A new study found that LEGO sets may actually be a pretty decent investment, as their value skyrockets after a few years when they cease being manufactured. Vindication!

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at [email protected] or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!