Silvergate Bank lost more than $8 billion in deposits from its crypto customers in the final months of 2022 as its core block of business crumbled under the industry’s implosion – just as the bank’s regulators had predicted might happen for such institutions.

The sudden evaporation of most of its deposit base was only one of several worries for the La Jolla, California-based lender. The company has faced pressures from U.S. banking watchdogs that have been insisting that banks shouldn’t concentrate on crypto, and its disclosures this week revealed investigations from regulators and the U.S. Department of Justice, plus a suggestion that ongoing audits may require a restating of its financials.

Apart from all that, its one-time crypto strengths were starting to drag it down, according to a CoinDesk analysis of the bank’s financial reports over the past several years.

(Kevin Ross/CoinDesk)

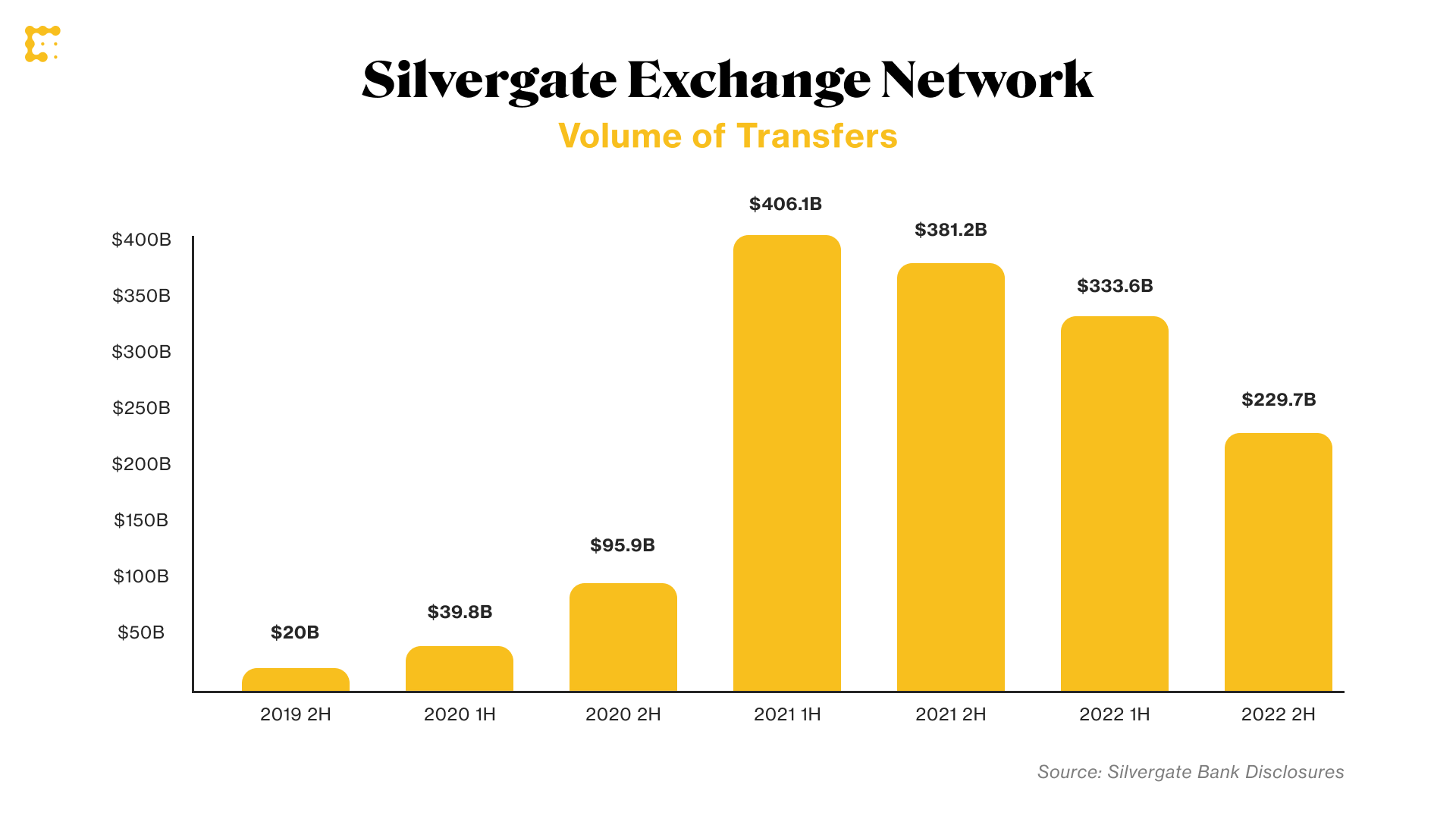

Many of the raw numbers reported by Silvergate over the years reveal an institution that may have peaked in 2021, well before the dramas of 2022 shook the crypto sector. The volume on its Silvergate Exchange Network, for instance, hit a high in the first half of 2021, with $406 billion in transfers, which slid to $230 billion by the second half of 2022.

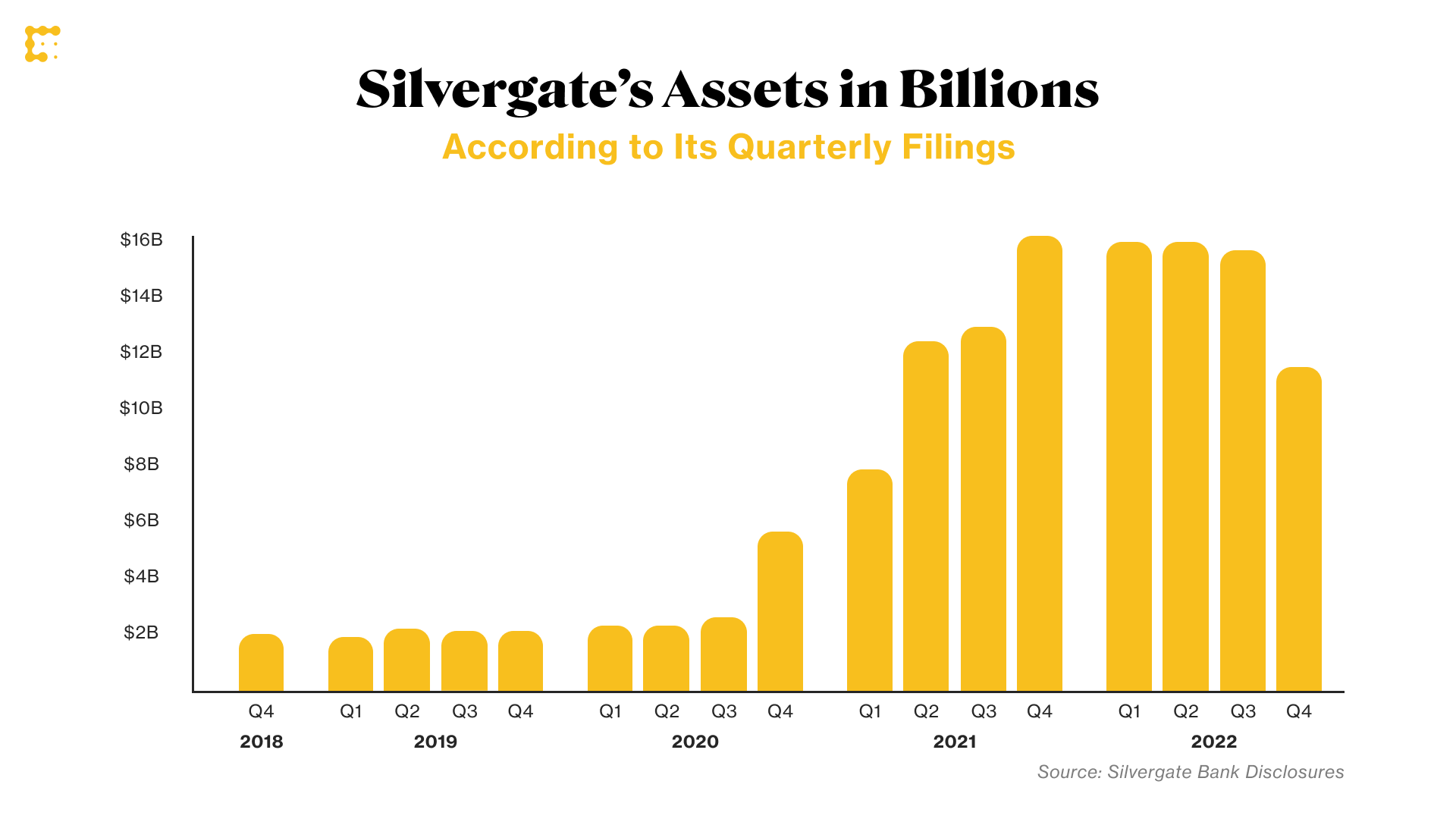

And the bank’s overall asset size also reached a high point in the fourth quarter of 2021, at $16 billion. Its most recent report showed it at $11.4 billion.

Even the high point of its assets describe a very small bank – the scale of a mid-range community bank – despite its outsized reputation as a core part of the digital assets industry’s U.S. banking presence. A near equivalent for its size in California would be the slightly larger Farmers and Merchants Bank of Long Beach, according to state banking data.

(Kevin Ross/CoinDesk)

But one key difference between Silvergate and the more traditional Long Beach community bank is in the key measure of their capital. The crypto bank slid rapidly into the final quarter of 2022 to a so-called leverage ratio that revealed it maintained just 5.4% of capital against its overall assets. In the same quarter at the latter bank, it reported a ratio of 10.9%.

According to U.S. bank capital rules, 5% is the edge of the cliff, beyond which a bank descends below a “well-capitalized” designation and toward the territory of emergency intervention from regulators.

A spokesman representing the bank said, “Silvergate can’t comment beyond what’s already been made publicly available.”

One of the most dramatic descents to track in Silvergate’s publicly released data was its deposits problem.

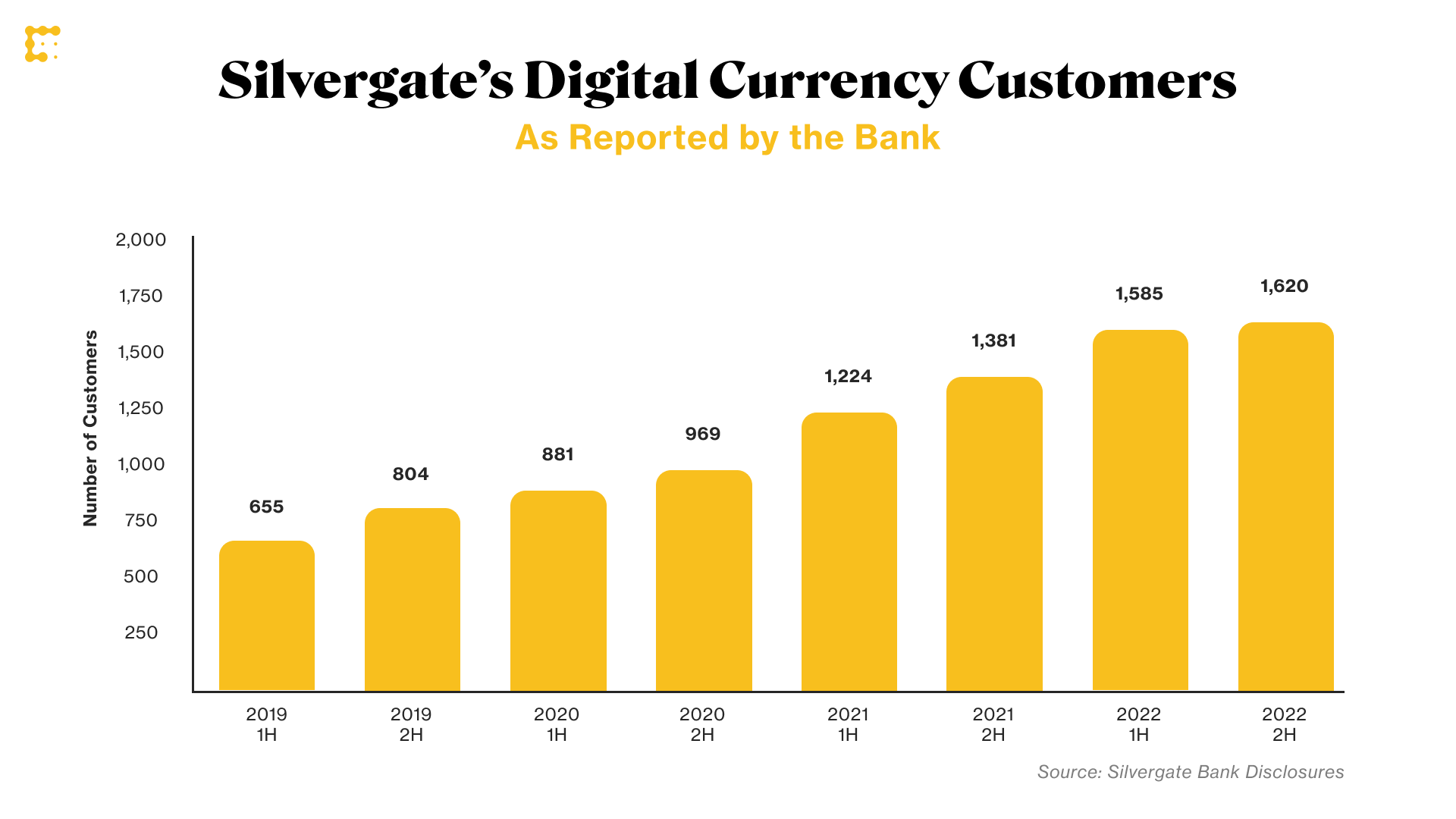

Silvergate identified the number of digital-assets customers it was working with each quarter, and that crowd steadily rose to 1,620 last quarter – most of those identified as institutional investors, though more than 100 were “digital asset exchanges.” However, those crypto customers’ deposits plummeted from almost $12 billion in the third quarter last year to less than $4 billion by the end of the year.

(Kevin Ross/CoinDesk)

The amount has clearly dropped much more than that now, as several big names in its customer base are severing ties. Coinbase, Paxos, Circle Internet Financial and Galaxy Digital have been among those making very public comments distancing themselves from the struggling bank.

A traditional, regulated depository institution can’t make it without a deposit base, and Silvergate’s coffers were drawn down quickly as major crypto clients dealt with their own collapses, bankruptcies and legal disputes that required an instant vacuuming of their liquid cash last year.

Still, for crypto businesses, the options for U.S. banking are getting narrower as the Federal Reserve and other banking agencies warn that they don’t want the lenders they oversee getting overly exposed to the digital assets sector. Only a few banks had been as openly and unapologetically crypto-focused as Silvergate, so its struggles aren’t offering a shining path for other institutions to follow.