Key derivatives market metrics show that sophisticated traders are turning their attention to ether (ETH) from the recent market standout, bitcoin (BTC), hinting at a potential outperformance of Ethereum’s native token in the coming weeks.

Bitcoin has rallied over 60% this quarter, while ether, the supposedly deflationary currency with bond-like appeal and ESG-compliant label, has lagged big time, gaining 35%, CoinDesk data show. The performance gap is even wider in larger time frames, with bitcoin boasting a 163% gain versus ether’s 89%.

The chasm could narrow as money is now flowing into ether futures faster than bitcoin. The notional open interest, or the dollar-value locked in Chicago Mercantile Exchange’s cash-settled ether futures contract, has increased by 30% to $711 million in the past five days, beating bitcoin’s 19% growth to $4.9 billion, according to Velo Data. CME’s ETH standard futures contract is sized at 50 ETH while its bitcoin counterpart is sized at 5 BTC.

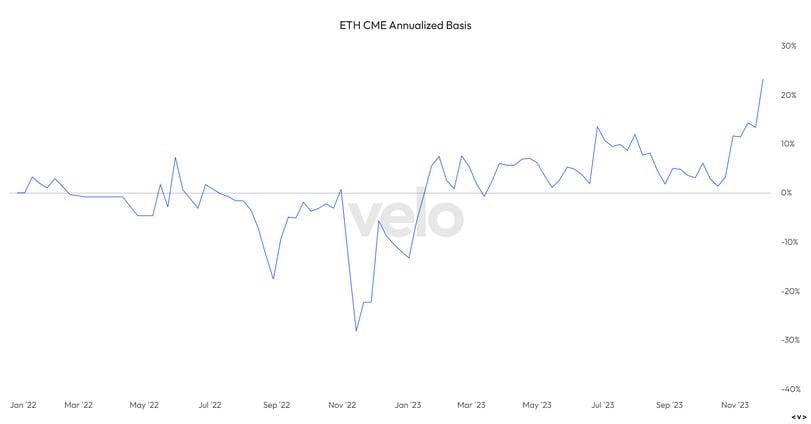

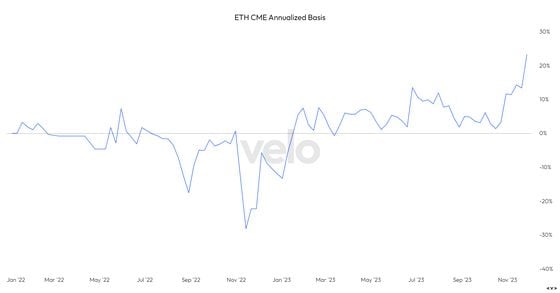

The emerging positive spread between pricing for ether and bitcoin CME futures suggests the same. Per Reflexivity Research, the premium in ether futures relative to the spot index price was 5% higher than in bitcoin early this week.

“The futures basis (which represents the difference between the spot and futures price) for Ethereum on CME is now trading at a 5% premium to that of bitcoin, now over 20%. In addition, we can see that open interest for ETH on the CME has now started to rise, after lagging the initial move up from bitcoin,” Reflexivity Research said in a market update dated Dec. 5.

“It may be too early to definitely say, but it appears ‘tradfi’ may be beginning to rotate into the ETH ETF trade after two months. This is something to continue monitoring for early signs of the market beginning to front-run a potential ETH ETF,” Reflexivity Research said.

Basis refers to the spread between futures and spot prices. (Velo Data) (Velo Data)

Meanwhile, in the options market listed on Deribit, traders have started to lean toward ether calls and bitcoin puts. A call option offers the right but not the obligation to purchase the underlying asset at a predetermined price at a later date. A call buyer is implicitly bullish on the market, while a put buy is bearish.

Per Amberdata, the one-month ether call-put skew, which measures the spread between implied volatility premium or demand for call and put options expiring in four weeks, has doubled to over 4% this month, a sign of strengthening call bias. Meanwhile, BTC’s one-month skew has declined from 5% to 2%, a sign that traders are beginning to lean toward puts relative to calls.

Perhaps bitcoin may take a breather, allowing ether to play catch up in the weeks ahead.