The U.S. Securities and Exchange Commission rejected more spot bitcoin exchange-traded fund applications. It’s worth unpacking the agency’s reasoning, even as new applications are filed.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

One step closer?

The narrative

Two bitcoin exchange-traded fund (ETF) applications were denied last week. The big question for me is whether we’re learning anything new from these rejections. At this point, I’m not sure – a lot of these rejections really read the same.

Why it matters

Even if the bitcoin ETF rejections are all similar, it’s always worth digging in and seeing what the Securities and Exchange Commission’s reasoning is, and what we can learn from it.

Breaking it down

To no one’s surprise, the Securities and Exchange Commission (SEC) rejected yet more bitcoin ETF applications, this time by Grayscale Investments and Bitwise Asset Management.

Grayscale almost immediately filed a petition for review with the DC Court of Appeals, asking the federal court system to take a look at the SEC’s decision and either declare it is with the Administrative Procedures Act or possibly just remand the decision back to the SEC but asking it to take another look at the application and review its process as to whether or not the rejection complied with its internal processes.

Disclosure: Grayscale and CoinDesk share a parent company in Digital Currency Group. CoinDesk remains editorially independent of all DCG companies.

The SEC reiterated its at this point very frequent concerns that there is the potential for market manipulation, that the stablecoin Tether (USDT) might be used to manipulate the market and that it does not believe that Grayscale or its partner, the NYSE Arca exchange, have met their obligations to reassure the SEC that this is not possible.

For its part Grayscale says that the approval of bitcoin futures ETF products should indicate that a spot market-based ETF product is safe for consumers. In the words of Grayscale Chief Legal Officer Craig Salm, like products should receive like treatment.

To better understand the SEC’s rejection, we should probably take a look at the Teucrium futures ETF approval. Now this is the bitcoin futures ETF that was filed under the same law that all the spot ETF applications have been filed under. When it was approved earlier this year, a lot of bitcoin ETF advocates said they believed it was a sign that the SEC might actually be willing to budge on the spot bitcoin applications.

The reasoning is this: SEC Chair Gary Gensler said last year that he was comfortable with futures ETFs filed under a specific law because that law enshrined certain consumer protections. The law that will govern spot bitcoin ETFs does not have the same protections.

In approving a futures ETF filed under the other law, the SEC opened the door to a spot ETF under that law, these advocates said.

(I’m keeping things relatively simple and vague – these are the 40 and 33/34 Acts, respectively, for those of you curious.)

The Teucrium approval also addressed the market manipulation concerns, saying:

“As Arca states, as a Designated Contracts Market … the CME ‘comprehensively surveils futures market conditions and price movements on a realtime and ongoing basis in order to detect and prevent price distortions, including price distortions caused by manipulative efforts.’ Thus the CME’s surveillance can reasonably be relied upon to capture the effects on the CME bitcoin futures market caused by a person attempting to manipulate the proposed futures ETP by manipulating the price of CME bitcoin futures contracts, whether that attempt is made by directly trading on the CME bitcoin futures market or indirectly by trading outside of the CME bitcoin futures market. As such, when the CME shares its surveillance information with Arca, the information would assist in detecting and deterring fraudulent or manipulative misconduct related to the non-cash assets held by the proposed ETP.”

In other words, the SEC believes that the CME can identify futures market manipulation regardless of how it’s attempted, even if the CME futures market is based on the price of bitcoin in some spot markets.

As a footnote in the Teucrium approval notes, “the CME CF BRR aggregates the trade flow of major bitcoin spot platforms during a specific calculation window into a once-a-day reference rate of the U.S. dollar price of bitcoin.”

At the same time, the SEC says it does not believe that the CME’s specific surveillance tools would be able to identify manipulation of the spot market “even if the Exchange or the Sponsor had demonstrated a link between the BRR and/or the Index and the prices of CME bitcoin futures ETFs/ETPs and/or the proposed ETP, which they have not.”

Once again, we must turn to the footnotes for the real juice. In footnote 46 of the Teucrium order, the SEC states that its reasoning in approving a futures ETF based on the CME’s ability to spot futures market manipulation “does not extend to spot bitcoin ETPs. Spot bitcoin markets are not currently ‘regulated.’”

In other words, Gensler may indeed be holding the bitcoin ETF “hostage” in an effort to bring crypto exchanges under his agency’s regulatory umbrella.

So what does all this mean for the Grayscale appeal? Meh, who knows. The company’s staffed up and prepared for this in recent weeks, bringing on former Solicitor General Don Verrilli and having an appeal letter ready to go pretty much immediately.

Christopher LaVigne, a litigation partner at the law firm Withers, told CoinDesk that “Grayscale’s in an uphill battle here,” saying the law tends to be “deferential” to the SEC.

“It’s just whether they made that decision and exercised that discretion in a way that was completely arbitrary, completely capricious and had no grounding in the law,” he said. “I think that’s a hard standard to meet and it’s intentionally a deferential standard. Otherwise, all federal agencies’ decisions would be constantly second guessed and they’d be subject to an unending amount of litigation.”

Bloomberg Intelligence’s James Seyffart pointed out that other industries do have ETFs despite a regulated spot market during a Twitter Space we held last week.

“There’s equity markets that the ISG does not have surveillance sharing agreements with, that we have ETFs for,” he said. “My overarching view is more so that the the SEC and Gary Gensler are holding these applications hostage until he can get regulation of the underlying spot market.”

So the next question may be what this actually looks like – it’s hard to see Congress moving swiftly to clarify when or how a crypto trading platform must register as a national securities exchange, and the SEC itself has yet to publish any proposed rulemaking on the matter.

Cheyenne Ligon contributed reporting.

Markets in Crypto Assets legislation

The European Union’s landmark Markets in Crypto Assets regulation is essentially a done deal now. Jack Schickler explains:

Last week was a big news week in the EU. The bloc’s Council and Parliament, the two bodies that need to agree on new laws, have done just that twice over – for a landmark Markets in Crypto Assets Regulation (MiCA), and for identity checks on crypto payments. The latter is intended to stamp out money laundering, but with big consequences for privacy – and is an implementation of the international Travel Rule that’s proved so hard to apply in the crypto space.

The final deals seem to have steered clear of some near misses that had plenty of crypto companies sweating. In the end, the laws don’t ban the proof-of-work technology that underpins bitcoin, or impose endless checks on transfers to self-hosted wallets, or force decentralized finance players to register with the authorities (and who would fill out the form, anyway?)

In principle, MiCA offers a sweet deal to crypto companies – who, in exchange for jumping through the EU’s hoops, get to market their wares across the bloc, which is one of the biggest economies in the world. But there’s still some pretty major questions over exactly who will have to sign up to the new system, and whether stablecoin rules that are designed to avoid collapses like terraUSD’s might strangle the market all together. In particular, there’s a lot of confusion about what the MiCA deal means for NFTs – and whether platforms like OpenSea will have to seek a license as the EU seeks to curb wash trades and other market abuses.

As the first major jurisdiction in the world to have such a comprehensive law, officials reckon they’re setting the tone for the rest of the world, and establishing the EU as the home of sound crypto. With the U.S. contemplating its own legislation on the issue, the bloc may not keep its lead very long.

CoinDesk reported both deals from the Room Where It Happened, here and here.

Read more: Here’s What Still Needs to Happen Before the EU’s MiCA Bill Becomes Law

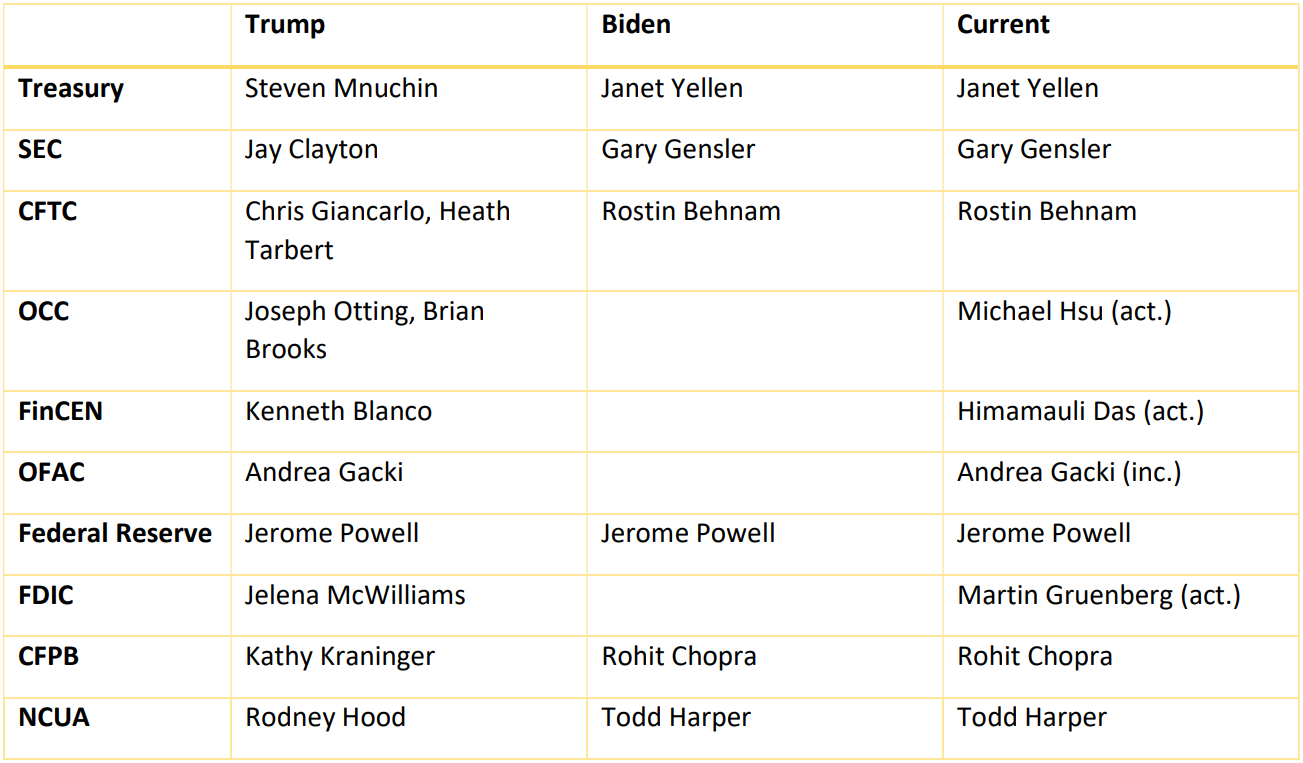

Biden’s rule

Changing of the guard

Key: (nom.) = nominee, (rum.) = rumored, (act.) = acting, (inc.) = incumbent (no replacement anticipated)

Fed Vice Chair for Supervision nominee Michael Barr is inching closer to a vote from the Senate.

Elsewhere:

-

Biden Official Says US Government Could Pass Stablecoin Rules by End of Year: There is so much I want to unpack on the legislative front, but that’ll have to wait for another time. For now: An official in the administration tells me there’s some real movement toward possible legislation on stablecoins by the end of 2022, though no specifics have emerged yet.

-

Three Arrows Paper Trail Leads to Trading Desk Obscured Via Offshore Entities: Three Arrows Capital was tied to an over-the-counter trading desk called Tai Ping Shen Capital, according to company documents. Sam Reynolds dives into this relationship and what it means for Three Arrows’ money.

-

Here’s What Still Needs to Happen Before the EU’s MiCA Bill Becomes Law: The European Union is closer to implementing its landmark Markets in Crypto Assets (MiCA) bill, but there’s a few steps left. Jack Schickler explains.

-

Voyager Seeks Bankruptcy Protection Amid Crypto Credit Crisis: Crypto broker Voyager Digital has filed for bankruptcy. More on this next week.

-

Genesis Faces ‘Hundreds of Millions’ in Losses as 3AC Exposure Swamps Crypto Lenders: Sources: Genesis Trading is facing a nine-figure loss due to overexposure to Three Arrows and Babel Finance. (Disclosure: Genesis is another DCG subsidiary.)

Outside CoinDesk:

-

(Bloomberg) Bloomberg takes a look at Heather Morgan (a.k.a. Razzlekhan) and Ilya Lichtenstein and asks whether they really could be the hackers behind Bitfinex’s 2016 theft.

-

(Trail of Bits) The Defense Advanced Research Projects Agency (DARPA) contracted Trail of Bits to take a look at how blockchains might be vulnerable. Interestingly, they found that underlying infrastructure providers (read: ISPs) may be a bigger threat vector than just node operators. The report is worth a read.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at [email protected] or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!